Internal Audit System

INVESTOR RELATIONS

Purpose

The purpose of Internal Audit is to assist the Board of Directors and management in reviewing and assessing deficiencies in the internal control system, evaluating operational effectiveness and efficiency, and providing timely recommendations for improvements. This ensures the continued effectiveness of the internal control system and serves as a basis for its review and enhancement.

Functions of the Internal Audit System

- Internal audit is an integral part of the internal control system, focused on assessing its effectiveness, evaluating operational performance, and providing timely improvement recommendations to ensure continued and effective implementation of the system.

- The internal audit aims to support the Board of Directors and management by identifying deficiencies in the internal control system and assessing operational efficiency. It also provides recommendations for improvements and serves as a basis for reviewing and refining the system.

- To fulfill its role, internal audit personnel are granted complete autonomy to audit all operational conditions and records within the company.

System Framework

- Review the internal control system to evaluate the effectiveness of existing policies and procedures, as well as their impact on business operations.

- Define the audit scope, timeline, procedures, and methodologies.

Scope of Application

- The Audit Unit and its deputies shall conduct audits in accordance with the relevant provisions of these guidelines.

- Audit subjects include all company departments, branches, and subsidiaries.

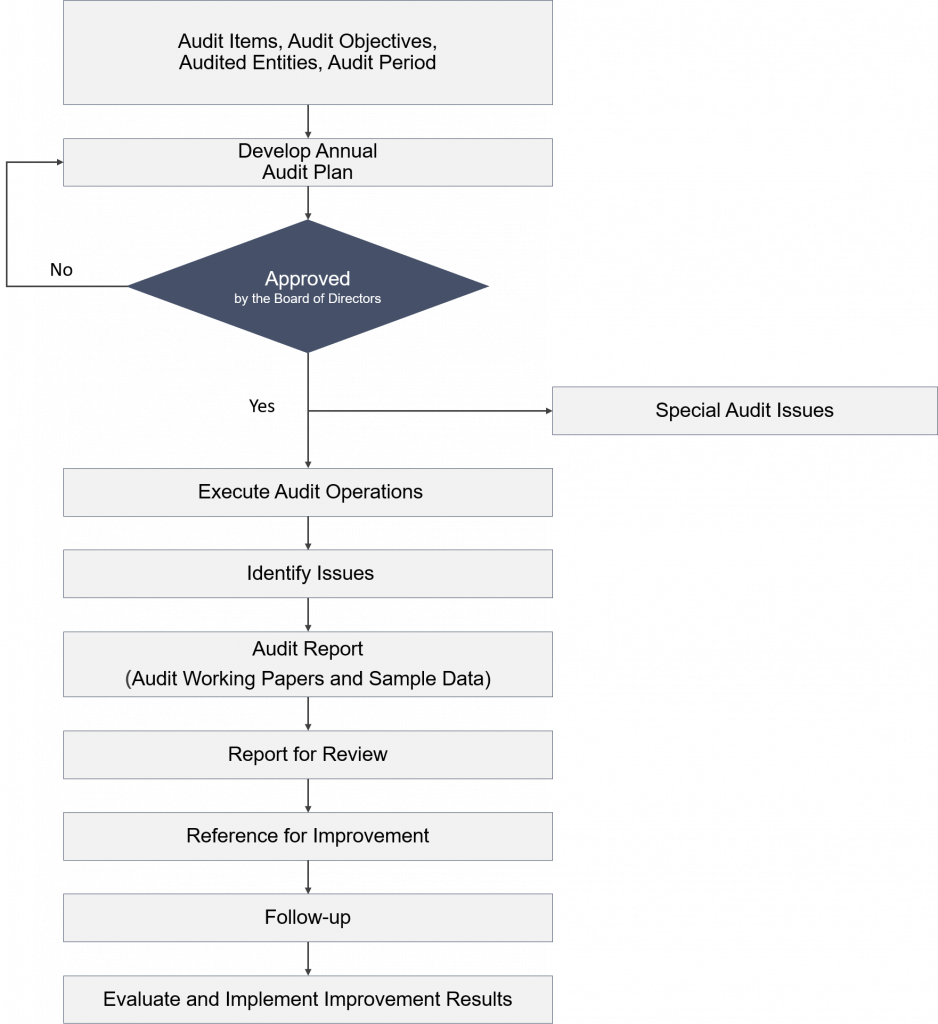

- Internal audits are categorized into regular and special (project-based) audits. Regular audits follow the Annual Audit Plan, while special audits are conducted as instructed by the Board of Directors (or the Audit Committee) or senior management.

Audit Process Flowchart